The famous RRSP. The perfect account for your investments because of the tax deductions and credits available to you. The RRSP can also become a source of considerable financial headaches when used improperly, especially when you exceed the RRSP limit. Penalties can be costly.

If you’ve inadvertently found yourself in this situation, don’t worry. There are a few ways to reduce or even waive the penalties.

RRSP contribution limits

The maximum you can contribute to your RRSPs is based on several factors. There are two ways to find out how much you should not exceed.

1. The hard way: by doing the math

- Your maximum permitted from last year

- +18% of your income for the year

- – Box 20 of your T4

- – Box 52 of your T4

- + the minimum HBP repayment requirement

- + the minimum refund required for the LLP

- – previous contributions made in the year

- – undeducted contributions from previous years

- – $2,000

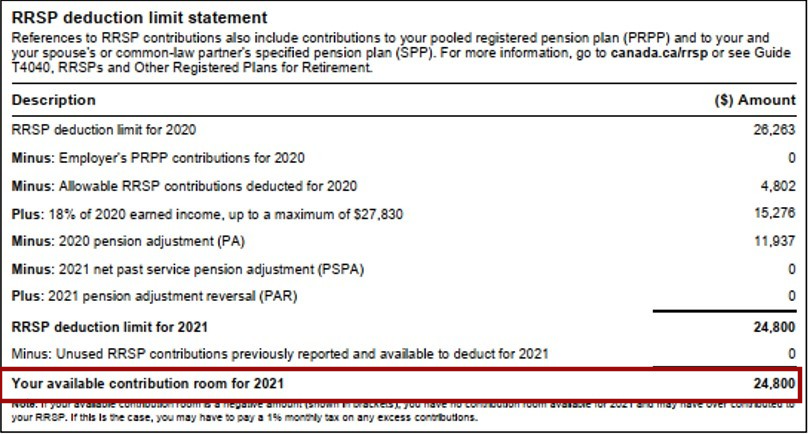

2. The simple way: Your Federal notice of assessment on page 3

Surplus contributions

You may make contributions up to $2,000 above the maximum allowed. Below that amount, the contribution is not deductible and no penalty is applied.

However, contributing more than $2,000 above the maximum allowed will result in two types of penalties:

- Special tax of 1% per full month on the amount over $2000

- Penalty of 1% per month of the special tax if the T1-OVP form has not been filed

Let’s see it with a specific example.

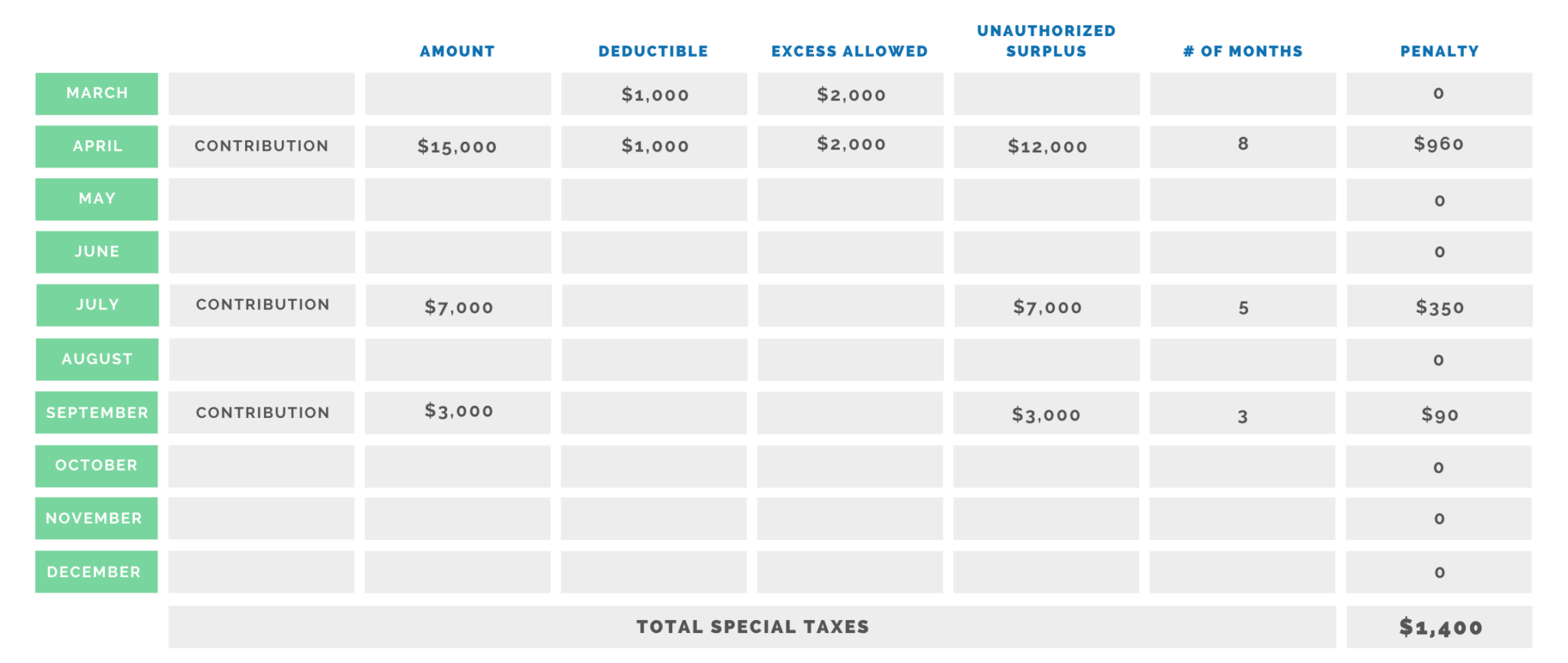

Luca’s example

Lucas’ notice of assessment is showing a maximum RRSP contribution of $1,000. But Lucas likes RRSPs too much and contributed $25,000 during the year thinking he would get a big tax refund. $15,000 in April, $7,000 in July and $3,000 in September.

The first $1000 is deductible on his next tax return. An excess of $2.000 is allowed before the special tax is applied.

Lucas will then have to pay $1,400 in special taxes. In addition, he must notify the CRA via a T1-OVP before March 31st of the next year to avoid an additional penalty of $14/month.

Some ways to avoid or reduce penalties

Withdrawal

If you catch the error of over-contributing quickly. The easiest solution administratively would be to withdraw the excess amount. However, expect your financial institution to withhold taxes from your income. These withholding taxes will still be recovered by filing your tax return the following year.

Alternatively, it is possible to apply to the CRA to have the institution not withhold taxes. The administrative process for this method, however, is not the easiest and delays can take months.

Early repayment of HBP or LLP

If you have an HBP or LLP balance, you can indicate a payment that exceeds the annual minimum required when you file your tax return.

This solution is even more interesting if the excess contribution has been present for several years. It is possible to adjust one or more previous years to compensate.

Request to cancel penalties

You can also ask the CRA to cancel these penalties through a written request. You must explain the reasons for the over-assessment. Your reasons must be reasonable to the officer who will be processing your file.

And of course, reasonableness can vary from person to person.

Looking for tax advice about your RRSPs? Our accountants can help.

Tax declaration Services for Companies